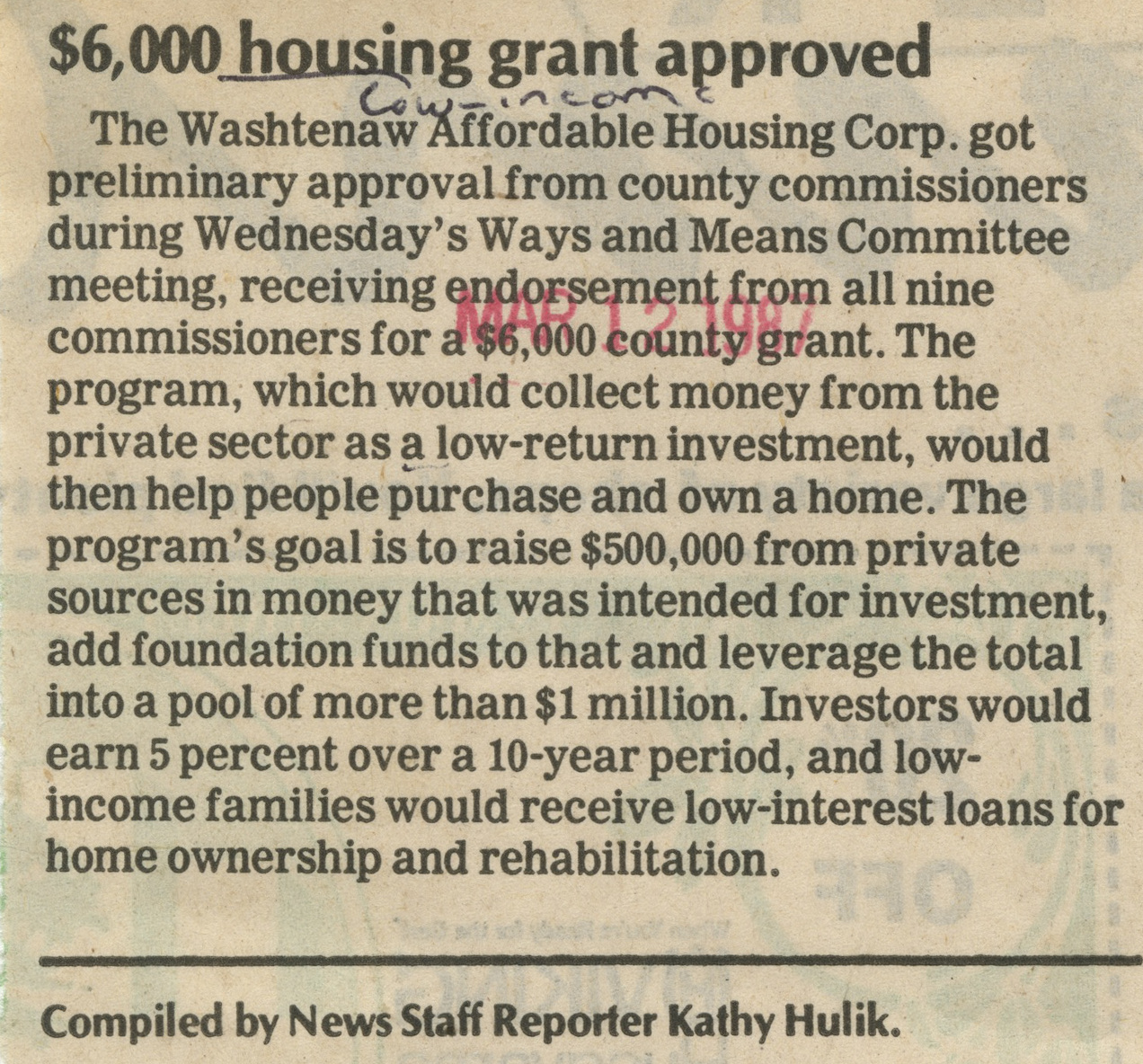

A study of the site Borrowing from the bank Sesame learned that the average few years the typical American resides in a property features enhanced out-of half a dozen in order to 9 many years because homes crisis

- What is the current rates, and you can what’s the index? (The new directory is determined from the sector forces, like the London area Interbank Offered Price, or LIBOR.)

A study by the website Borrowing from the bank Sesame found that the new average long-time the typical American lives in property provides improved from six so you can nine many years since the homes drama

- What’s the margin because of it mortgage? (This is actually the financial earnings put in the latest index.)

A survey by the webpages Borrowing Sesame discovered that the average few years an average American lives in a house have enhanced from half dozen to nine many years since the construction drama

- The length of time does the first price history, and just how commonly is also the pace to improve?

A study from the website Borrowing from the bank Sesame found that the new average number of years the typical Western resides in a property provides enhanced from half dozen to 9 ages because property drama

- What are the occasional attract-speed hats, additionally the life desire-rate cover? (This can reveal just how highest the rate might have to go.)

Of a lot changeable-price funds are derived from brand new several-day LIBOR, hence, as of late Will get, are 0.55 per cent, according to HSH study. The typical margin simultaneously are dos.25 percent. It is therefore not unusual to own the present Palms to-fall towards the 2.75 percent to three percent variety. This is why regardless of if rates into the conventional 29-year repaired rates finance in the was hovering regarding the cuatro.twenty-seven percent in order to 4.31 percent range, simply a lot more than the lowest accounts in the a production, of many Hands be a little more appealing as they promote even lower pricing.

Over the years, the common You.S. homebuyer holds a mortgage for approximately half a dozen or eight years and you may next dumps that loan while they promote the house or refinance. More recently, though, customers seem to be hanging on to its mortgages for longer symptoms.

This is exactly why, when it comes to Fingers, Gumbinger states delivering such finance isn’t just a question of “visitors beware,” however, alot more an instance of “customer see thyself,” if you want to improve best mortgage choice.

Gumbinger claims when anyone fifty or elderly provides this regular circumstances – state, five in order to seven ages out-of today the children is out of college or university as well as the members of the family won’t need a giant house in https://cashadvancecompass.com/loans/200-dollar-payday-loan/ the the fresh new suburbs – next an effective 5/1 Sleeve otherwise 7/step 1 Sleeve would be worthwhile considering. Centered on recent studies from HSH, costs for 5/step one Arms across the country is actually close to step 3 %. Cost into seven/step one Possession is somewhat large, within step 3.cuatro percent.

“Although simple truth is, many people do not truly know where they get into 5 years otherwise 7 age,” Gumbinger says.

Often it comes down to that it question: “How well are you presently which have and come up with preparations for the future and you will following adhering to him or her?” Gumbinger asks. “And are also you prepared in the event it does not work aside for you? Because if your own preparations changes, their mortgage need change also.”

cuatro. Hedge the bet

Pros are practically unanimous within their convinced that – just after a lot of several years of suprisingly low rates of interest – rates can just only go a proven way in the near future: upwards. Should you choose a supply, manage specific “let’s say” projections.

“Estimate where you can easily start by the borrowed funds, what’s the bad-case scenario you could potentially find, including a functional within the-the-middle circumstance,” Gumbinger claims.

When you crisis the fresh wide variety, decide if you will be able to handle the mortgage from the different membership. At the least, you need to be in a position to move the new midrange monetary projection to own the Case. Otherwise, reconsider the borrowed funds.

In the event that refinancing with the a supply lowers your own mortgage payment from the, state, $eight hundred or $five-hundred 1 month, save your self that money inside an alternative account you don’t reach. At the least by doing this, you build a financial back-up to simply help counterbalance and prepare into big date later on when the and if higher monthly money are present. “Even when we obtain back once again to just what are a great deal more typical cost – of about 7 per cent to eight % – that would be extremely shameful for almost all consumers who’ve getting always to three per cent otherwise 4 percent cost,” Gumbinger states. Therefore, the more money support your attain you will definitely offset some of one to economic blow.