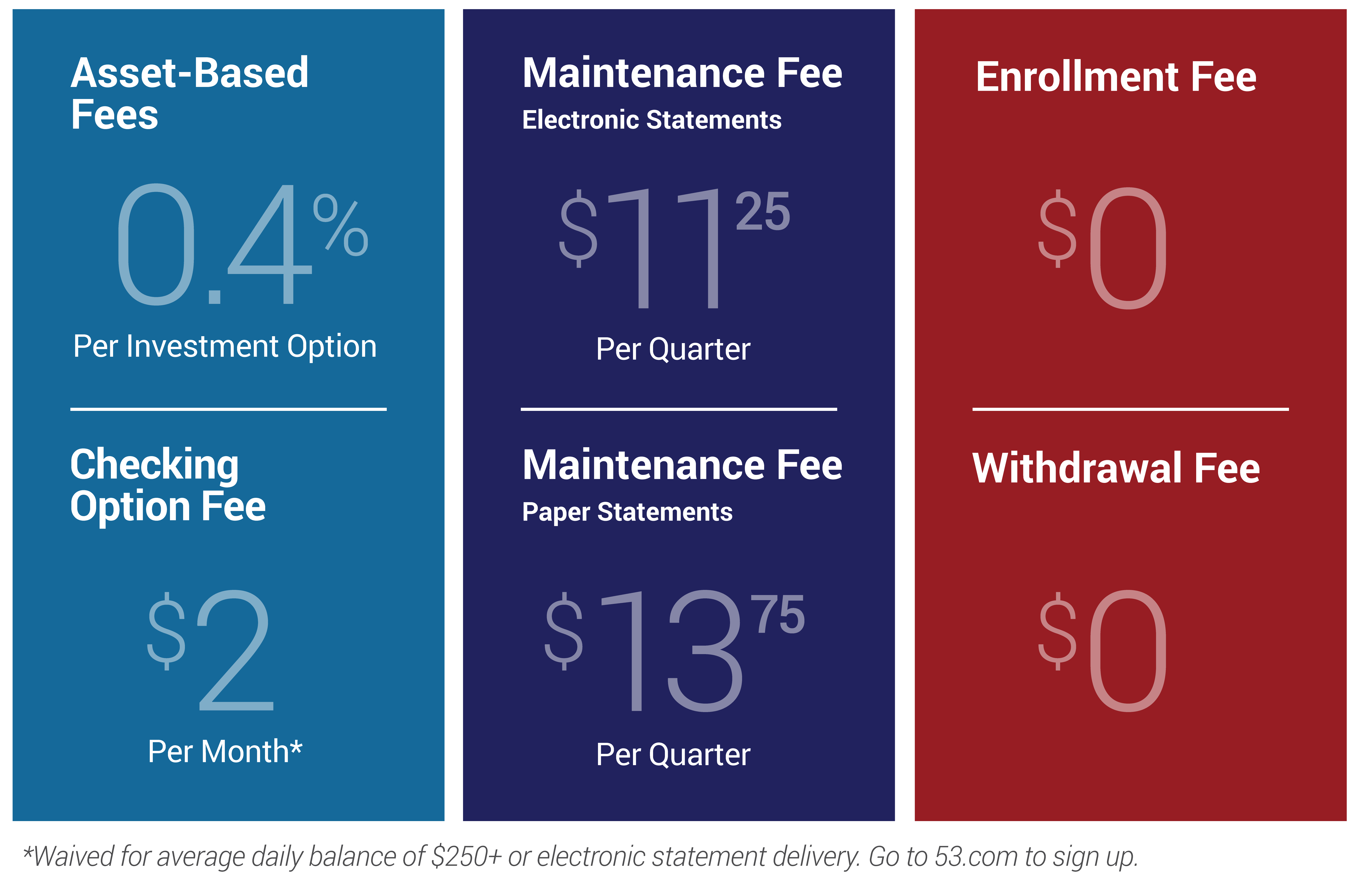

A home loan is one of the most significant monetary purchases you are able to ever before create and remaining such as highest financial obligation affordable generally involves lowering your interest. Knowing the difference between both chief sort of mortgage loans – compliant and you can non conforming mortgage – helps you accomplish that.

The explanation for a couple of various other financial models

Having one or two financial classes helps reduce home financing lender’s risk. Anytime a loan provider will bring financing, they deal with considerable chance. Should your borrower defaults, the lending company should endure a long (and you may pricey) property foreclosure way to recover your debt. To cut back their overall exposure, loan providers are selling their house loans so you’re able to a few bodies-backed people:

- Federal national mortgage association (Fannie mae)

- Freddie Mac (Government Mortgage Home loan Organization)

Fannie and you will Freddie simply undertake mortgages you to satisfy many standards; however, it is the money number of the mortgage that is the unmarried very important aspect for the determining if or not financing is actually conforming home loan otherwise non conforming financial.

Compliant mortgages

This new conforming-financing maximum for one house is now $417,000, although this restriction is good over the continental You. For the Alaska, Hawaii, Guam, and the U.S. Virgin Countries, the fresh new restriction try $625,five hundred.

For as long as their home loan will not surpass the fresh maximum for your area, you’ve got a compliant mortgage. These types of mortgage loans are attractive due to their lower rates of interest.

There are many situations – besides the conforming-financing maximum – the place you may not meet the assistance put by Fannie and you may Freddie. Any of these products is:

- Loan-to-worth proportion exceeds ninety%

- Debt-to-earnings ratio is higher than forty five% of the monthly pre-taxation income (including monthly home loan repayments, insurance policies, taxes or any other unsecured instant same day payday loans online Illinois debt repayments)

- Obligations is recognized as chock-full of regards to your earnings

- Credit history try below 620 or if you enjoys a woeful credit history

- Credit score shows a recently available bankruptcy proceeding

- Software is destroyed data files, like your employment background, listing of property or earnings facts

Non-compliant mortgage loans

Funds one to exceed $417,000 (or $625,five hundred beyond your all the way down forty eight) are generally also known as jumbo money. These types of non-conforming loans are used to purchase high-listed characteristics, eg luxury number 1 residences otherwise second house. A non compliant home loan normally allow you to secure investment to own a home which you if you don’t may possibly not be capable pick.

Loan providers try faster pretty sure regarding the probability they can be able to sell a non-compliant home loan. They offset that it risk from the recharging higher rates. At the same time, a non-compliant loan you will are most other initial costs and you may insurance coverage-relevant standards. If you are considering a low conforming financial, always take action homework whenever choosing a loan provider.

Shortly after understanding different sorts of mortgage loans, just be able to concentrate on the professionals that come with each. To sum it up, is a run down of your own key features of conforming and you may non conforming mortgages.

- Down rates of interest

Choosing that’s most suitable for you between compliant and you will non compliant finance utilizes various products that were not limited by the total amount becoming loaned as well as your economic situation. To make certain that you will be securely directed in selecting the proper financial, seek the assistance of financial experts.

When you find yourself in search of qualified advice and assistance on your own financial, think Carlyle Financial. As home financing financial, we are able to give you multiple alternatives around a great unmarried roof. We are a primary lender who will procedure, agree and you may money their financial for the-family. You can expect a publicity-100 % free feel, regardless if you are buying your first or your upcoming house.

Contact us at to start cultivating a romance that have a loan provider who knows your needs and will be offering your having choice customized so you’re able to your preferences. If you enjoy the genuine convenience of our safe on the web mode, you can get already been right here. A home loan banker often get in touch with you soon to discuss your residence mortgage choice.