If places would much better than We expect any kind of time part along the twenty-five-seasons title, then i is also option out-of using more to help you paying off the attention-merely mortgage till the financial obligation becomes due, and maybe even deploy lump figures liquidated from my ISAs against the loan (even when it’s difficult for me to conceive to do that and shedding the my beloved ISA wrapper…)

New Accumulator altered his attention when you look at the the same-ish condition and you may chose to work with reducing his mortgage debt in lieu of maximising his using increases. Zero guilt in this!

2. You’re not reducing the financial support you can easily fundamentally owe

The second also sophisticated conflict is the fact paying, say, ?400,000 is actually a giant slog for most people, and you may you’ll be best off creating early.

Adhering to my personal ?400,000/dos.5% example (and you can rounding getting easier studying) in the first season out of a fees mortgage might pay ?nine,860 when you look at the appeal. You’ll only pay off ?eleven,666 of your a great financial support.

Brand new data do get most readily useful through the years. By the seasons 10 you may be paying off ?fourteen,610 per year inside resource, that have less than ?seven,000 going on interest. Simply because your earlier payments possess shrunk your debt that notice is due to the.

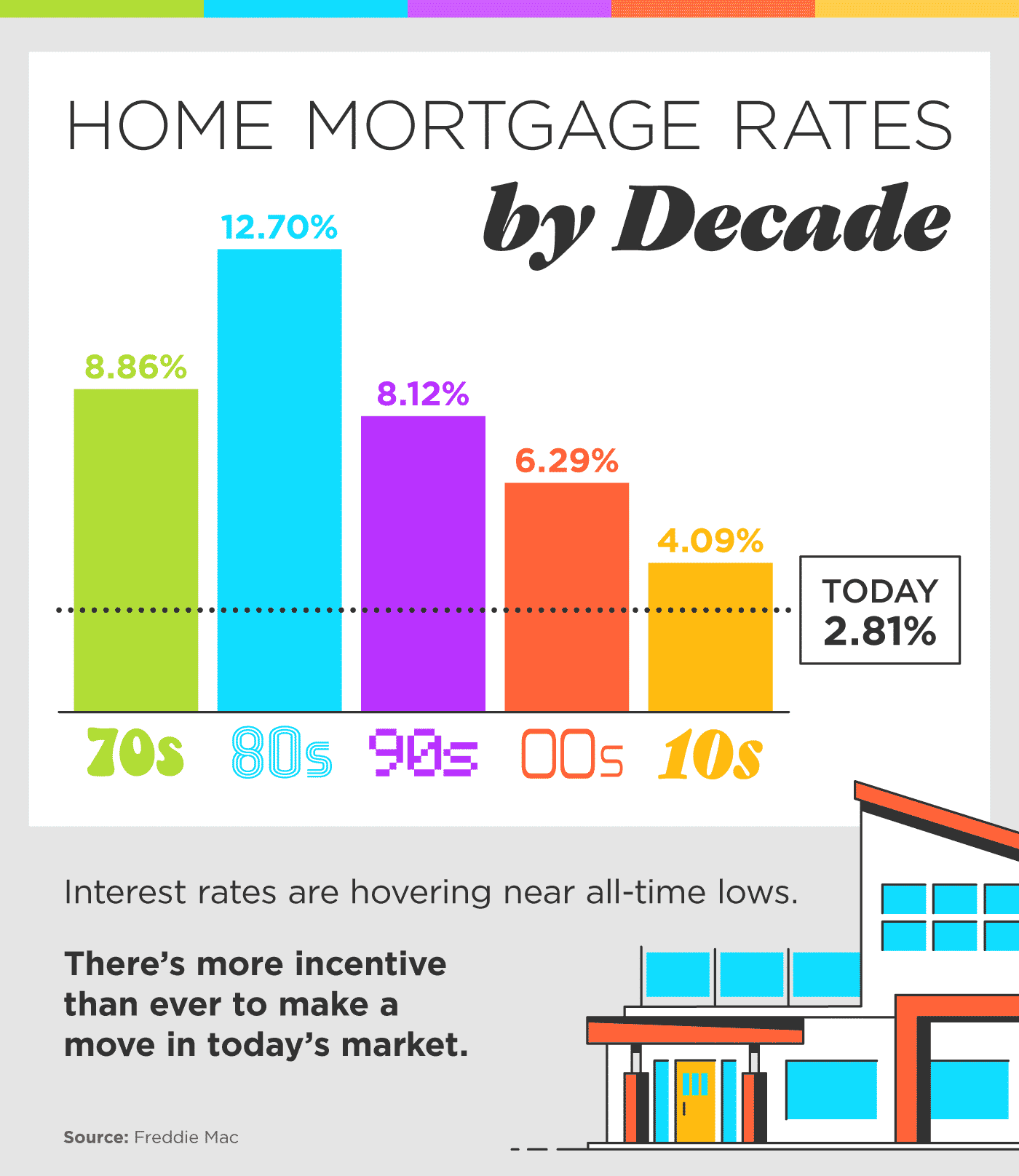

At an even more typically normal financial rate from six%, you’d spend almost ?24,000 within the demand for year that on that ?eight hundred,000 mortgage, and simply ?7,000 of money.

Here’s an example of the attention/financial support separated not as much as an excellent 6% program. See how much time it will take to possess money payments in order to provide more benefits than focus payments:

Without a doubt we do not currently reside in a six% techniques. You might argue that which have the current lower pricing is in reality a great blast to possess a fees financial in order to slashed the long-label obligations, just because most of the money are getting on the funding.

It is simply sometime concealed, since when a bank rents your money to acquire a house, it-all gets wrapped right up in one single payment.

step three. You’re not smoothing out your property exposure

The stock exchange seems shaky, so instead of spending I’ll earn some additional money towards my personal financial to help you set a lot more into the assets markets alternatively. You simply can’t go wrong which have domiciles!

I have even got a friend recommend in my opinion one to paying off their mortgage through the years (and additionally with over-payments) feels as though pound-costs averaging on stock exchange.

After you buy a property is when you earn your own exposure’ towards the housing market. Your visibility moving forward is the property you bought. The cost of that house ‘s the rates your paid off whenever you bought it.

All of pnc personal loan pre approved us pull out a mortgage to purchase our house. How we will shell out one to off every month to your lifetime of the loan or perhaps in you to lump sum inside the twenty five years, or something like that during the-between is mostly about dealing with financial obligation, not altering our possessions exposure.

If one makes a supplementary ?fifty,000 payment to your financial, you haven’t got ?fifty,000 much more exposure to brand new housing industry. Your residence visibility has been almost any your property is well worth.

How to lb-pricing average on the residential property marketplace is to purchase multiple characteristics throughout the years, or even to put money into a loft extension otherwise comparable.seven

cuatro. What if you simply cannot improve attention money you may not individual your property?

Someone frequently trust having fun with an interest-simply home loan is much more precarious than simply a payment financial. Your may see that it insinuated in posts.

You will find a feeling that somebody staying in property financed that have home financing in which they’re not repaying obligations monthly try living on the a limb.